UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K/A

(Amendment No. 1)

ý ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2013

OR

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to .

Commission File Number: 1-8944

CLIFFS NATURAL RESOURCES INC.

(Exact Name of Registrant as Specified in Its Charter)

|

| | |

Ohio | | 34-1464672 |

(State or Other Jurisdiction of Incorporation or Organization) | | (I.R.S. Employer Identification No.) |

| |

200 Public Square, Cleveland, Ohio | | 44114-2315 |

(Address of Principal Executive Offices) | | (Zip Code) |

Registrant’s Telephone Number, Including Area Code: (216) 694-5700

Securities registered pursuant to Section 12(b) of the Act:

|

| | |

Title of Each Class | | Name of Each Exchange on Which Registered |

Common Shares, par value $0.125 per share | | New York Stock Exchange and Professional Segment of NYSE Euronext Paris |

Depositary Shares, each representing a 1/40th ownership interest in a share of 7.00% Series A Mandatory Convertible Preferred Stock, Class A | | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

NONE

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES ý NO ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. YES ¨ NO ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES ý NO ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). YES ý NO ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ý Accelerated filer ¨ Non-accelerated filer ¨ Smaller reporting company ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). YES ¨ NO ý

As of June 28, 2013, the aggregate market value of the voting and non-voting common shares held by non-affiliates of the registrant, based on the closing price of $16.25 per share as reported on the New York Stock Exchange — Composite Index, was $2,577,942,533 (excluded from this figure is the voting stock beneficially owned by the registrant’s officers and directors).

The number of shares outstanding of the registrant’s common shares, par value $0.125 per share, was 153,181,056 as of April 28, 2014.

DOCUMENTS INCORPORATED BY REFERENCE - NONE

EXPLANATORY NOTE

This Amendment No. 1 on Form 10-K/A ("Form 10-K/A") to the Annual Report on Form 10-K of Cliffs Natural Resources Inc. for the fiscal year ended December 31, 2013, originally filed with the Securities and Exchange Commission ("SEC") on February 14, 2014 (the "Original 10-K"), is being filed solely for the purpose of including the information required by Part III of Form 10-K. References in this Form 10-K/A to the “Company,” “we,” “us,” “our” and “Cliffs” are to Cliffs Natural Resources Inc. and its subsidiaries, collectively. The Company, which usually holds its annual meeting of shareholders in May, no longer anticipates filing its definitive proxy statement within 120 days of its fiscal year ended December 31, 2013. Therefore, such information will not be incorporated by reference from the Company's definitive proxy statement for the 2014 annual meeting of shareholders. Thus, Part III, Items 10-14, of the Company's Original 10-K are hereby amended and restated in their entirety.

Pursuant to Rule 12b-15 under the Securities Exchange Act of 1934, this Form 10-K/A also contains new certifications by the principal executive officer and the principal financial officer as required by Section 302 of the Sarbanes-Oxley Act of 2002. Accordingly, Item 15(a)(3) of Part IV is amended to include the currently dated certifications as exhibits. Because no financial statements have been included in this Form 10-K/A and this Form 10-K/A does not contain or amend any disclosure with respect to Items 307 and 308 of Regulation S-K, paragraphs 3, 4 and 5 of the certifications have been omitted.

Except as described above, this Form 10-K/A does not modify or update disclosure in, or exhibits to, the Original 10-K. Furthermore, this Form 10-K/A does not change any previously reported financial results, nor does it reflect events occurring after the date of the Original 10-K. Information not affected by this Form 10-K/A remains unchanged and reflects the disclosures made at the time the Original 10-K was filed.

TABLE OF CONTENTS |

| | | | | |

| | | | | |

| | | Page Number |

| | | | | |

PART III | | | |

| Item 10. | Directors, Executive Officers and Corporate Governance | | | |

| Item 11. | Executive Compensation | | | |

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | | | |

| Item 13. | Certain Relationships and Related Transactions, and Director Independence | | | |

| Item 14. | Principal Accountant Fees and Services | | | |

| | | | | |

PART IV | | | |

| Item 15. | Exhibits and Financial Statement Schedules | | | |

| | | |

SIGNATURES | | | |

Part III

|

| |

Item 10. | Directors, Executive Officers and Corporate Governance |

DIRECTORS OF THE COMPANY

The Board of Directors (the "Board") currently consists of eleven members. Each director was elected to serve until the 2014 annual meeting of shareholders (the "2014 Annual Meeting") or until their successors shall be elected.

Susan M. Cunningham - First Became Director: 2005; Independent, Age 58, Senior Vice President, Gulf of Mexico, Africa and Frontier Ventures and Business Innovation of Noble Energy Inc., an international oil and gas exploration and production company, since April 2013. Ms. Cunningham served as Senior Vice President of Exploration from May 2007 to April 2013 and Senior Vice President of Exploration and Corporate Reserves of Noble Energy Inc. from 2005 to May 2007. Ms. Cunningham brings to the Board years of global exploration, geology, major project, operations and energy experience from her various roles with Noble Energy Inc. As we have grown internationally and expanded into mineral exploration and through mining acquisitions (metallurgical coal and chromite, as examples), her guidance has been a valuable asset to our Board in assessing the value of exploration and acquisition projects as well as providing guidance when we address energy usage and carbon-related issues. Committee Assignments: Governance and Nominating Committee and Strategy and Sustainability Committee. Ms. Cunningham’s leadership skills, developed as a senior executive of an international public company, are an asset to our Governance and Nominating Committee. Ms. Cunningham’s global exploration, operations and strategy experiences and knowledge and understanding of global mining and exploration industries and reserve calculations strengthen our Strategy and Sustainability Committee. Ms. Cunningham’s executive experience is also a valuable resource for Cliffs’ Board in its dealings with senior management.

Barry J. Eldridge - First Became Director: 2005; Independent, Age 68, Currently retired. Mr. Eldridge previously served as the Managing Director and Chief Executive Officer of Portman Limited, an international iron ore mining company in Australia, from October 2002 through April 2005. Mr. Eldridge formerly served as chairman of Vulcan Resources Ltd. from 2005 to 2008, chairman of Millennium Mining Pty. Ltd. from 2007 to 2008 and chairman of Mundo Minerals Limited until 2012. He currently serves as a director of Sundance Resources Ltd. All of these companies are or were listed on the Australian Stock Exchange. As a former executive of an international mining company and former chairman of various Australian mining companies, Mr. Eldridge brings to the Board a wealth of international management experience as well as business perspectives specific to the Australian coal and iron mining industry, which is one of Cliffs’ strategic focuses. Committee Assignments: Strategy and Sustainability Committee (Chair) and Compensation and Organization Committee. Mr. Eldridge’s extensive international mining and exploration expertise is an asset to our Strategy and Sustainability Committee, particularly when evaluating new strategic opportunities. His management experience both on boards of other companies and as a former executive facilitates his ability to lead as Chair of the Strategy and Sustainability Committee and strengthens the Compensation Committee through his understanding of compensation strategies necessary to retain and attract international exploration and mining talent.

Mark E. Gaumond - First Became Director: 2013; Independent, Age 63, Currently retired. Mr. Gaumond previously served as the Senior Vice Chair - Americas of Ernst & Young LLP, a global leader in assurance, tax, transaction and advisory services, from 2006 to 2010. Previously he served as Ernst & Young's Managing Partner, San Francisco from 2003 to 2006 and as an audit partner on several major clients. Prior to joining Ernst & Young, Mr. Gaumond was a partner with a 27-year career with Arthur Andersen LLP. Mr. Gaumond serves on the Boards of Directors and Audit Committees of Rayonier, Inc. and Booz Allen Hamilton Holding Corporation. He is also a director and president of the Fishers Island Development Corporation and a director of the Walsh Park Benevolent Corporation. He is a former trustee of the California Academy of Sciences. Mr. Gaumond has more than 35 years of managerial, financial and accounting experience working extensively with senior management, audit committees and board of directors of public companies. His experience in financial accounting and reporting, compliance and internal controls, and public company audit committee experience allow him to contribute to our Board's oversight of the Company's overall financial performance, reporting and controls. Committee Assignments: Audit Committee and Compensation and Organization Committee. Mr. Gaumond’s extensive financial reporting and accounting background combined with his organizational management skills strengthens our Audit Committee and Compensation Committee. The Board has identified Mr. Gaumond as a financial expert under SEC regulations.

Andrés R. Gluski - First Became Director: 2011; Independent, Age 56, President and Chief Executive Officer of The AES Corporation ("AES"), a Fortune 200 company and one of the world’s largest independent power producers

with operations in 26 countries, since 2011. Prior to assuming the role of CEO, Dr. Gluski was Executive Vice President and Chief Operating Officer of AES from 2007 to 2011. Dr. Gluski currently serves on the Boards of Directors of AES, AES Gener S. A., the Edison Electric Institute, the Council of the Americas/Americas Society, the U.S. - Brazil CEO Forum and the U.S. Spain Council. In 2013, he was named by President Obama to serve on his Export Council. Previously, Dr. Gluski worked with the International Monetary Fund and served as director general of the Ministry of Finance in Venezuela. Dr. Gluski’s years of managing large capital intensive projects and businesses in the U.S. and abroad provide the Board with valuable experience and knowledge in dealing with numerous issues. Committee Assignments: Audit Committee and Strategy and Sustainability Committee. Dr. Gluski’s background in international finance and economics along with his knowledge of the power industry brings practical expertise to both committees on which he serves. The Board has identified Dr. Gluski as a financial expert under SEC regulations.

Susan M. Green - First Became Director: 2007; Independent, Age 54, Currently retired. Ms. Green previously served as Deputy General Counsel, U.S. Congressional Office of Compliance from November 2007 through September 2013. She originally was proposed as a nominee for the Board by the United Steelworkers (the "USW") pursuant to the terms of our 2004 labor agreement. Ms. Green has served as both a labor organizer and as an attorney representing organized labor. She also has worked in the Legislative and Executive Branches of the federal government, including six years as Deputy General Counsel of the Office of Compliance, which enforces the labor and employment laws for the Legislative Branch, and her prior position as Chief Labor Counsel for then-Senator Edward M. Kennedy, as well as several positions in the U.S. Department of Labor during the Administration of President Bill Clinton. She brings her diverse experiences as a labor attorney and an alternative point of view to our Board. As someone who has represented organized labor, she is able to advocate the views of the majority of our North American workforce. Committee Assignments: Audit Committee and Governance and Nominating Committee. Ms. Green’s labor and governmental background brings practical experience to both committees.

Gary B. Halverson - First Became Director: 2013; Management, Age 55, President (since November 2013) and Chief Executive Officer (since February 2014) of Cliffs. Mr. Halverson was elected as President & Chief Operating Officer of Cliffs effective November 18, 2013 and as Chief Executive Officer of Cliffs effective February 13, 2014. Prior to joining Cliffs, Mr. Halverson served as Interim Chief Operating Officer from September 2013 to November 2013, as President-North America from December 2011 to November 2013 and as President-Australia Pacific from December 2008 to December 2011 for Barrick Gold Corporation Inc. ("Barrick"), an international gold mining company. Mr. Halverson brings a global mining perspective with experience in a variety of minerals, including gold, copper and nickel, to the Board. Recently, he provided leadership for the largest gold region in the world at Barrick. Through his serving in various capacities in mining operations internationally, he has experience managing large annual operating budgets and capital projects. These experiences include a wide range of underground and open-pit mines from the construction and development phases through the end-of-life stage.

Janice K. Henry - First Became Director: 2009; Independent, Age 63, Currently retired. Ms. Henry previously served as Senior Vice President from 1998 through June 2006, Chief Financial Officer from 1994 to June 2005 and Treasurer from 2002 to March 2006 of Martin Marietta Materials, Inc. ("Martin Marietta"), a producer of construction aggregates serving the public infrastructure, commercial and residential construction markets in the U.S. Ms. Henry served in a consulting capacity for Martin Marietta from July 2006 through June 2009. Ms. Henry was a director of North American Galvanizing & Coatings, Inc. from February 2008 through August 2010. In January 2012, Ms. Henry became a director of W.R. Grace & Co., a global specialty chemicals and materials company, and serves on its audit and compensation committees. Since October 2009, Ms. Henry has been a member of The Charles Stark Draper Laboratory, Inc., a nonprofit corporation, which engages in activities that contribute to the support and advancement of scientific research, technology and development. Ms. Henry’s background with Martin Marietta brings significant accounting, financial, SEC reporting, risk analysis and audit experience to our Board. As a former director on the boards of Inco Limited and North American Galvanizing & Coatings, Inc., Ms. Henry contributes her board-level experience and background in mining and basic materials. Committee Assignments: Audit Committee (Chair) and Compensation and Organization Committee. Ms. Henry’s extensive financial reporting and accounting background provides the additional expertise required for audit committees of public companies. Cliffs’ Board has determined that she is a financial expert (as that term is defined in SEC regulations) on the Audit Committee. Additionally, her financial background complements the activities of the Compensation Committee and she is an important link between the Audit and Compensation Committees.

Stephen M. Johnson - First Became Director: 2013; Independent, Age 62, Currently retired. Mr. Johnson previously served as Chairman, President and CEO of McDermott International, Inc., a U.S.-based engineering and construction company focused exclusively on the upstream offshore oil and gas sector with global operations, from July 2010 through December 2013. Mr. Johnson was elected Chairman of McDermott’s board of directors in May 2011. Previously, Mr. Johnson served as President and Chief Executive Officer of its subsidiary, J. Ray McDermott, S.A.,

from January 2010 to July 2010 and as President and Chief Operating Officer of McDermott International, Inc. from April 2009 to December 2009. Before joining McDermott, he held the position of Senior Executive Vice President and Member, Office of the Chairman at Washington Group International, prior to its sale to URS Corporation. Having served as a chairman and CEO of a public engineering and construction company, Mr. Johnson presents to our Board valuable insight into operational management issues crucial to a large public company and that relate to large development projects. Committee Assignments: Audit Committee and Governance and Nominating Committee. As a former Chairman, President and CEO of a NYSE-listed company, he understands the financial reporting requirements of a public company and is well versed in the mechanics of corporate governance issues.

James F. Kirsch - First Became Director: 2010; Management, Age 56, interim executive Chairman of Cliffs, since January 2014. Mr. Kirsch previously served as Chairman, President and CEO of Ferro Corporation ("Ferro"), a global supplier of technology-based materials for a broad range of manufacturers, until November 2012. Mr. Kirsch was elected Chairman of Ferro’s board of directors in December 2006 and appointed CEO and a director of Ferro in November 2005. Mr. Kirsch joined Ferro in October 2004 as its President and Chief Operating Officer. Prior to joining Ferro from 2002 through 2004, Mr. Kirsch served as President of Premix Inc. and Quantum Composites, Inc., manufacturers of thermoset molding compounds, parts and subassemblies for the automotive, aerospace, electrical and HVAC industries. From 2000 through 2002, he served as President and director of Ballard Generation Systems, a company engaged in the design, development, manufacture and sale of clean energy fuel cell products, and Vice President for Ballard Power Systems in Burnaby, British Columbia, Canada. Mr. Kirsch brings a wealth of senior management experience with major organizations with international operations. As a former Chairman, President and CEO of a NYSE-listed company, he brings additional chairmanship and CEO experience to Cliffs’ Board and the committees on which he serves. Mr. Kirsch, as a former chairman and CEO of a public company with global operations, contributes to the Board a full range of strategic management expertise and a broad understanding of the issues facing an international business.

Richard K. Riederer - First Became Director: 2002; Independent, Age 70, Chief Executive Officer of RKR Asset Management, a consulting organization, since June 2006. Mr. Riederer served as President and CEO from January 1996 through February 2001 of Weirton Steel Corporation, a North American steel producing company. Mr. Riederer has been a director of First American Funds since September 2001. He also serves on the Board of Trustees of Franciscan University of Steubenville. Mr. Riederer’s long career in the steel industry as well as his experience as CEO and Chief Financial Officer of Weirton Steel Corporation brings executive management, accounting and finance and financial reporting expertise to Cliffs’ Board as well as an in-depth knowledge of the North American steel industry. His insight as past chairman of North American Iron & Steel Institute is invaluable. Committee Assignments: Governance and Nominating Committee (Chair) and Strategy and Sustainability Committee. Mr. Riederer’s strong sense of leadership and knowledge of the steel industry supports the purpose of our Strategy and Sustainability Committee. His experience as a former and current director on other boards enhances his role as Chair of the Governance and Nominating Committee.

Timothy W. Sullivan - First Became Director: 2013; Independent, Age 60, Chairman and CEO of Gardner Denver Inc., a manufacturer of products for energy, industrial and medical applications, since July 2013. Mr. Sullivan previously served as Executive Advisor to CCMP Capital Advisors LLC, a private equity firm, from 2012 to 2013. He also served as President, CEO and a director of Bucyrus International Inc., a surface and underground mining equipment company from 2004 until 2011 and President from 2000 to 2004. In 2012, he served as a special consultant to Wisconsin Governor Scott Walker and he chaired the Governor's Council on Workforce Investment and the College of Workforce Readiness Council. He currently chairs the Wisconsin Mining Association and he is a director of Aurora Health Care, Inc. and Northwestern Mutual Life Insurance Company. As a former President and CEO of a company that manufactures mining equipment, Mr. Sullivan brings to the Board a unique perspective about the mining industry. Committee Assignments: Compensation and Organization Committee (Chair) and Strategy and Sustainability Committee. As a current and former CEO, Mr. Sullivan has significant leadership experience and strategic management expertise, and he understands the compensation strategies necessary to attract and retain talented employees.

EXECUTIVE OFFICERS OF THE REGISTRANT

Following are the names, ages and positions of the executive officers of the Company as of April 28, 2014. Unless otherwise noted, all positions indicated are or were held with Cliffs Natural Resources Inc.

James F. Kirsch, Age 56, Chairman of the Board and interim executive Chairman of Cliffs (January 2014-present); non-executive Chairman of the Board (July 2013-December 2013); Director (March 2010-present); and Chairman (December 2006-November 2012); President and Chief Executive Officer (November 2005-November 2012) of Ferro, a global supplier of technology-based materials for a broad range of manufacturers.

Gary B. Halverson, Age 55, Director, President and Chief Executive Officer (Feb. 2014-present); Chief Operating Officer (November 2013-February 2014); Interim Chief Operating Officer (September 2013-November 2013), President-North America (December 2011-November 2013), and President-Australia Pacific (December 2008-December 2011) for Barrick, an international gold mining company.

William C. Boor, Age 48, Executive Vice President, Corporate Development & Chief Strategy Officer (February 2014-present); Senior Vice President, Strategy & Business Development (July 2013-February 2014); Senior Vice President, Global Ferroalloys (January 2011-July 2013); President - Ferroalloys (May 2010-January 2011); and Senior Vice President, Business Development (May 2007-May 2010).

Terry G. Fedor, Age 49, Executive Vice President, United States Iron Ore (January 2014-present); Vice President (February 2011 - January 2014); Vice President and General Manager (March 2005 - February 2011) of ArcelorMittal Cleveland, a fully integrated steelmaking facility, which included oversight for Weirton, Warren, Monessen and Lackawanna.

Terrance M. Paradie, Age 46, Executive Vice President (March 2013-present); Chief Financial Officer (October 2012-present); Senior Vice President (January 2011-March 2013); Assistant General Manager-Michigan Operations (March 2012-September 2012); Corporate Controller (October 2007-March 2012); Chief Accounting Officer (July 2009-March 2012); and Vice President (October 2007-January 2011).

Clifford T. Smith, Age 54, Executive Vice President, Seaborne Iron Ore (Jan. 2014-present); Executive Vice President, Global Operations (July 2013-January 2014); Executive Vice President, Global Business Development (March 2013-July 2013); Senior Vice President, Global Business Development (January 2011-March 2013); Vice President, Latin American Operations (September 2009-January 2011); and General Manager-Business Development (October 2006-September 2009) .

P. Kelly Tompkins, Age 57, Executive Vice President, External Affairs & President, Global Commercial (November 2013-present); Chief Administrative Officer (July 2013-November 2013); Executive Vice President, Legal, Government Affairs and Sustainability (May 2010-July 2013); Chief Legal Officer (January 2011-January 2013); President, Cliffs China (October 2012-November 2013); and Executive Vice President and Chief Financial Officer (June 2008-May 2010) of RPM International Inc., a specialty coatings and sealants manufacturer.

David L. Webb, Age 57, Executive Vice President (January 2014-present); Senior Vice President, Global Coal (July 2011-January 2014); and Vice President and General Manager of Mid-West Operations for Patriot Coal Corp., a producer of thermal and metallurgical coal (2007-June 2011).

Timothy K. Flanagan, Age 36, Vice President, Corporate Controller & Chief Accounting Officer (March 2012-present); Assistant Controller (February 2010-March 2012); and Director, Internal Audit (April 2008-February 2010).

James D. Graham, Age 48, Vice President (March 2012-present); Chief Legal Officer (March 2013-present); Secretary (March 2014-present); General Counsel (January 2011-March 2013); and Assistant General Counsel (March 2009-January 2011).

SECTION 16(a) BENEFICIAL OWNERSHIP REPORTING COMPLIANCE

Section 16(a) of the Exchange Act requires our directors and officers and persons who own more than 10 percent of a registered class of our equity securities to file reports of ownership and changes in ownership on Forms 3, 4 and 5 with the SEC. Directors, officers and greater than 10 percent shareholders are required by SEC regulations to furnish us with copies of all Forms 3, 4 and 5 they file.

Based solely on our review of the copies of such forms we have received, and written representations by such persons, we believe that, except as otherwise noted below, all of our directors, officers and greater than 10 percent

shareholders complied with all filing requirements applicable to them with respect to transactions in our equity securities during the fiscal year ended December 31, 2013. On February 26, 2013, a Form 4 for each of Laurie Brlas, Donald Gallagher and Terrence Mee that was reporting their respective vesting of performance shares on February 21, 2013 was filed a day late due to technical filing difficulties. Also on February 26, 2013, a Form 3/A was filed for Terrance Paradie to include restricted stock units that were inadvertently omitted from his original filing on October 9, 2012.

Board Meetings and Committees

During 2013, 14 meetings of Cliffs’ Board and a total of 41 meetings of Cliffs’ Board committees were held. Our independent directors held 12 meetings in executive session without the presence of Mr. Joseph A. Carrabba, our former Chairman, CEO and President, through November 2013. Mr. Francis R. McAllister served as Lead Director beginning May 2004 until his resignation in June 2013, at which time the Board appointed Mr. Kirsch as our Lead Director and then our Chairman of the Board. Messrs. McAllister and Kirsch chaired five and nine of the Board’s executive session meetings, respectively, in 2013. Directors also discharge their responsibilities by reviewing reports to directors, visiting our facilities, corresponding with the CEO, and conducting telephone conferences with the CEO and directors regarding matters of interest and concern to Cliffs. In addition, directors have regular access to senior management of Cliffs. The directors attend Audit, Governance and Nominating, Compensation and Organization, and Strategy and Sustainability Committee meetings as well as ad hoc committee meetings when needed.

All committees regularly report their activities, actions and recommendations to Cliffs’ Board. During 2013, one independent director attended at least 86 percent of the aggregate total of Cliffs' Board and committee meetings while the remaining independent directors attended at least 95 percent of the aggregate total of Cliffs’ Board and committee meetings. No director attended less than 75 percent of the aggregate total of Cliffs’ Board and committee meetings of which they were members.

Board Committee Membership

The Board of Directors has four standing committees: Audit, Compensation and Organization, Governance and Nominating and Strategy and Sustainability. The table below indicates the members of each committee as of July 1, 2013 through today except as noted below.

|

| | | | |

Director | Audit | Compensation & Organization | Governance & Nominating | Strategy & Sustainability |

Gary B. Halverson | | | | |

Susan M. Cunningham | | | ü | ü |

Barry J. Eldridge | | ü | | µ |

Mark E. Gaumond (1) | ü | ü | | |

Andrés R. Gluski | ü | | | ü |

Susan M. Green | ü | | ü | |

Janice K. Henry (2) | µ | ü | | |

Stephen M. Johnson (3) | ü | | ü | |

James F. Kirsch ¬ (4) | | | | |

Richard K. Riederer LD (5) | | | µ | ü |

Timothy W. Sullivan | | µ | | ü |

¬ Chairman of the Board LD Lead Director µ Committee Chair ü Member

| |

(1) | Mr. Gaumond has been a member of the Audit Committee and the Compensation Committee since his election to the Board effective in July 2013. |

| |

(2) | Ms. Henry became chair of the Audit Committee in April 2013 when Richard A. Ross resigned from the Board. |

| |

(3) | Mr. Johnson has been a member of the Audit Committee and the Governance and Nominating Committee since his election to the Board effective October 1, 2013. |

| |

(4) | Mr. Kirsch became our Lead Director when Francis McAllister retired from the Board in June 2013. In July 2013, Mr. Kirsch became our Chairman of the Board. In January 2014, Mr. Kirsch became our interim executive Chairman of the Board. |

| |

(5) | Since the time that Mr. Kirsch became our interim executive Chairman of the Board, Mr. Riederer, as Chair of the Governance & Nominating Committee, has been acting as our Lead Director when there are any conflicts while Mr. Kirsch serves as interim executive Chairman. |

Audit Committee. The Audit Committee reviews with our management, the internal auditors and the independent registered public accounting firm, the adequacy and effectiveness of our system of internal control over financial reporting; reviews significant accounting matters; reviews quarterly unaudited financial information prior to public release; approves the audited financial statements prior to public distribution; approves our assertions related to internal controls prior to public distribution; reviews any significant changes in our accounting principles or financial reporting practices; reviews, approves and retains the services performed by our independent registered public accounting firm; has the authority and responsibility to evaluate our independent registered public accounting firm; discusses with the independent registered public accounting firm their independence and considers the compatibility of non-audit services with such independence; annually selects and retains our independent registered public accounting firm to examine our financial statements; approves management’s appointment, termination or replacement of the Chief Risk Officer; and conducts a legal compliance review at least annually. The members of the Audit Committee are independent under applicable SEC rules and the NYSE listing standards. Cliffs’ Board has identified Messrs. Gaumond, Gluski, Johnson and Riederer and Ms. Henry as audit committee financial experts (as defined in Item 407(d)(5)(ii) of Regulation S-K of the SEC rules). No member of the Audit Committee serves on the audit committees of more than three public companies. The Audit Committee held 10 meetings during 2013. The charter of the Audit Committee is available at http://www.cliffsnaturalresources.com.

Governance and Nominating Committee. The Governance and Nominating Committee is involved in determining director compensation and reviews and administers our director compensation plans; monitors the Board governance process and provides counsel to the CEO on Board governance and other matters; recommends changes in membership and responsibility of Board committees; and acts as the Board’s Nominating Committee and Proxy Committee in the election of directors. The Governance and Nominating Committee held five meetings during 2013. The charter of the Governance and Nominating Committee is available at http://www.cliffsnaturalresources.com.

As noted above, the Governance and Nominating Committee is involved in determining compensation for our directors. The Governance and Nominating Committee reviews and administers our director compensation plans, and makes recommendations to the Board with respect to compensation plans and equity-based plans for directors. The Governance and Nominating Committee annually reviews director compensation in relation to comparable companies and other relevant factors. Any change in director compensation must be approved by Cliffs’ Board. Other than Mr. Kirsch in his capacity as a director, no executive officers participate in setting director compensation. From time to time, the Governance and Nominating Committee or Cliffs’ Board may engage the services of a compensation consultant to provide information regarding director compensation at comparable companies.

Compensation and Organization Committee. The Compensation and Organization Committee (the "Compensation Committee") recommends to Cliffs’ Board the election and compensation of officers; administers our executive compensation plans for officers; reviews management development; evaluates the performance of the CEO and the other executive officers; and obtains the advice of outside experts with regard to compensation matters. The Compensation Committee may, in its discretion, delegate all or a portion of its duties and responsibilities to a subcommittee.

The Compensation Committee obtains analysis and advice from an external compensation consultant to assist with the performance of its duties under its charter. The Compensation Committee directly retained Semler Brossy Consulting Group, or Semler Brossy, for 2013, and Semler Brossy helped the Compensation Committee develop an appropriate agenda for performing the Compensation Committee’s responsibilities. In this regard, Semler Brossy advised and assisted the Compensation Committee in determining the appropriate objectives and goals of our executive compensation programs; in designing compensation programs that fulfill those objectives and goals; in seeking to align executive compensation programs with shareholder interests; in evaluating the effectiveness of our compensation programs; in identifying appropriate pay positioning strategies and pay levels in our executive compensation programs; and in identifying mining industry and general industry peers and identifying compensation surveys for the Compensation Committee to use to benchmark the appropriateness and competitiveness of our executive compensation program.

The Compensation Committee makes all decisions regarding the President/CEO’s compensation, subject to ratification by the independent members of the Board, after consulting with its advisors in executive session where no management employees are present. For the other executive officers, the President/CEO is asked by the Compensation Committee to conduct and present an assessment on the achievement of specific goals established for those officers

and on Cliffs’ performance, taking into account external market forces and other considerations. While the President/CEO, Chief Financial Officer, or CFO, and Executive Vice President, Human Resources attend Compensation Committee meetings regularly by invitation, the Compensation Committee is the final decision maker for the compensation of the executive officers. For additional information regarding the operation of the Compensation Committee, see “Compensation Discussion and Analysis” beginning on page 13 of this Form 10-K/A. The Compensation Committee held seven meetings during 2013. The charter of the Compensation Committee is available at http://www.cliffsnaturalresources.com.

Strategy and Sustainability Committee. The purpose of the Strategy and Sustainability Committee is to oversee Cliffs’ strategic plan, annual management objectives and operations and to oversee and monitor risks relevant to its strategy, as well as operational, safety and environmental risks. The Strategy and Sustainability Committee provides advice and assistance with developing our current and future strategy; provides follow up oversight with respect to the comparison of actual results with estimates for major projects and post-deal integration; ensures that Cliffs has appropriate strategies for managing exposures to economic and hazard risks; assesses Cliffs’ overall capital structure and its capital allocation priorities; assists management in determining the resources necessary to implement Cliffs’ strategic and financial plans; monitors the progress and implementation of Cliffs' strategy; acts in an advisory capacity to the Board and management with respect to Cliffs’ global sustainability strategies and its social license to operate; and reviews the adequacy of Cliffs’ insurance programs. The Strategy and Sustainability Committee held seven meetings in 2013. The charter of the Strategy and Sustainability Committee is available at http://www.cliffsnaturalresources.com.

Business Ethics Policy

We have adopted a Code of Business Conduct and Ethics (the "Ethics Code"), which applies to all of our directors, officers and employees. The Ethics Code is available on our website at http://cliffsnaturalresources.com in the Corporate Governance section under "Investors". We intend to post amendments to or waivers from our Ethics Code (to the extent applicable to our principal executive officer, principal financial officer or principal accounting officer) on our website. Reference to our website and the contents thereof do not constitute incorporation by reference of the information contained on our website, and such information is not part of this Form 10-K/A.

Independence and Related Party Transactions

Our Board has determined that each of the current directors standing for re-election, other than Messrs. Halverson and Kirsch, and all of the current members of the Audit, Governance and Nominating, and Compensation Committees, have no material relationship with us (either directly or as a partner, shareholder or officer of an organization that has a relationship with us) and is independent within the NYSE director independence standards. The Board also determined that Messrs. McAllister and Ross, who served as directors during 2013, met these independence standards. Mr. Halverson is our President & CEO and Mr. Kirsch is our interim executive Chairman, and, as such, each is not considered independent. Messrs. Halverson and Kirsch do not serve as a member of any of Cliffs’ Board committees.

Since January 1, 2013, there have been no transactions or currently proposed transactions, in which Cliffs was or is to be a participant and the amount exceeds $120,000, and in which any related person had or will have a direct or material interest. We recognize that transactions between us and any of our directors or executive officers can present potential or actual conflicts of interest and create the appearance that our decisions are based on considerations other than the best interests of our shareholders.

We have a written Related Party Transactions Policy, pursuant to which we only will enter into related party transactions if our CEO and Chief Legal Officer determine that the transaction is comparable to those that could be obtained in arm’s length dealings with an unrelated third party. If the transaction is approved by our CEO and Chief Legal Officer, then the transaction also must be approved by the disinterested members of our Audit Committee. For purposes of our policy, we define a related person as any person who is a director, executive officer, nominee for director or an immediate family member of a director, an executive officer or a nominee for director. We define a related party transaction as a transaction, agreement or relationship in which Cliffs was, is or will be a participant, the amount of the transaction exceeds $120,000, and a related person has or will have a direct or indirect material interest. However, compensation paid by Cliffs for service as a director or executive officer of the Company is not deemed to be a related party transaction, even if the aggregate amount involved exceeds $120,000. Under our policy, any related party transactions are reviewed by the Audit Committee at each quarterly committee meeting.

We have entered into indemnification agreements with each current member of the Board. The form and execution of the indemnification agreements were approved by our shareholders at the Annual Meeting convened on

April 29, 1987. The indemnification agreements essentially provide that, to the extent permitted by Ohio law, we will indemnify the indemnitee against all expenses, costs, liabilities and losses (including attorneys’ fees, judgments, fines or settlements) incurred or suffered by the indemnitee in connection with any suit in which the indemnitee is a party or otherwise involved as a result of his or her service as a member of the Board. In connection with the indemnification agreements, we have a trust agreement with KeyBank National Association pursuant to which the parties to the indemnification agreements may be reimbursed with respect to enforcing their respective rights under the indemnification agreements.

In 2004, we reached an agreement with the USW pursuant to which the USW may designate a member to the Board provided that the individual is acceptable to the Chairman, is recommended by the Board Affairs Committee (now known as the Governance and Nominating Committee), and is then approved by the full Board to be considered a director nominee. In 2007, Susan Green was first proposed by the USW, elected to the Board by Cliffs’ shareholders in July 2007, and re-elected in each of the years 2008 through 2013.

|

| |

Item 11. | Executive Compensation |

DIRECTOR COMPENSATION

The directors who are not Cliffs’ employees receive a combination of cash and equity compensation. The table below sets forth the cash compensation fee schedules for the nonemployee directors in 2013 and what currently is in effect for 2014. In addition, customary expenses for attending Board and committee meetings are reimbursed. Employee directors receive no additional compensation for their service as directors. In July 2013, the Board replaced the Lead Director position with a nonemployee Chairman of the Board of Directors, who received a quarterly retainer of $125,000 for the remainder of 2013. In January 2014, the nonemployee Chairman became an interim executive Chairman of the Board of Directors.

|

| | | | |

Board Form of Cash Compensation | 2014($) | | 2013($) |

Annual Retainer | 100,000 | | 60,000 | |

Board Meeting Fees | Not applicable | | 2,000 | / meeting |

Committee Meeting Fees | Not applicable | | 1,500 | / meeting |

Chairman (non-executive) of the Board Annual Retainer | Not applicable | | 500,000 | |

Lead Director Annual Retainer | 40,000 (1) | | 40,000 | |

Audit Committee Chair Annual Retainer | 20,000 | | 20,000 | |

Compensation and Organization Committee Chair Annual Retainer | 12,500 | | 12,500 | |

Annual Retainers for Chairs of Governance and Nominating and Strategy and Sustainability Committees | 10,000 | | 10,000 | |

(1) The Lead Director Annual Retainer is not applicable to the extent an interim executive Chairman has been named.

Equity Grants. The directors’ annual equity grants are made under the Nonemployee Directors’ Compensation Plan (as Amended and Restated as of December 31, 2008), which we refer to as the Directors’ Plan. Effective May 8, 2012 and in accordance with the terms of the Directors’ Plan, $85,000 of restricted or unrestricted common shares, as described below, is awarded to each nonemployee director on the annual meeting date, unless otherwise determined by the Board. Nonemployee directors who are under age 69 on the date of the annual meeting receive an automatic annual grant of restricted shares with a three-year vesting requirement. Nonemployee directors who are 69 years of age or older on the date of the annual meeting receive an automatic annual grant of common shares (with no restrictions). Two directors (Messrs. McAllister and Riederer) received their annual equity award in the form of unrestricted shares in May 2013, and one (Mr. Riederer) will receive unrestricted shares in the 2014 annual equity grant. Any directors who joined the Board after the annual meeting held on May 7, 2013 (the "2013 Annual Meeting") received a prorated award of restricted shares pursuant to the Directors’ Plan. Directors receive dividends on their annual equity grants and may elect that all cash dividends with respect to restricted shares be deferred and reinvested in additional common shares. Those additional common shares are subject to the same restrictions as the underlying award. Cash dividends not subject to a deferral election will be paid to the director without restriction.

Effect of Share Ownership Guidelines. We have established Director Share Ownership Guidelines and assess each director’s compliance with the guidelines in December of each year. If a nonemployee director meets the guidelines as of that assessment date, the director may elect to receive all or a portion of his or her annual retainer

for the following year in cash. If the director does not meet these guidelines, the director is required to receive an equivalent value of a specified portion of the annual retainer in common shares until he or she meets the guidelines. For those directors who were required (or elected) to receive payment of their 2013 annual retainers in the form of common shares, $24,000 of the retainer paid during 2013 was paid in common shares. Whether or not they are required to receive part of their retainer as common shares, nonemployee directors may elect to receive up to 100 percent of their retainer and other fees in common shares. The cash portions of the annual retainers are paid quarterly, and common shares are issued at the beginning of the next fiscal year for the portion of each quarter’s retainer that is paid in common shares. Through 2013, directors were paid fees for attending meetings. However, since it is expected that directors will attend all meetings, effective January 1, 2014, directors will no longer receive meeting fees unless the number of meetings during a particular year are excessive, but rather will receive his or her annual retainer, which will be paid solely in cash.

The Director Share Ownership Guidelines that were in effect as of the December 2012 assessment, and which determined whether or not directors were required to receive a portion of their 2013 retainers in common shares, required each director to hold or acquire common shares having a market value of at least $250,000 within five years of becoming a director. The directors who did not hold the requisite value of common shares (Messrs. Gluski, Kirsch and Ross and Mses. Green and Henry), all of whom have been directors for less than five years, received at least a portion of their retainer in common shares in 2013.

Deferrals. The Directors’ Plan gives nonemployee directors the opportunity to defer all or a portion of their annual retainer and other fees, whether payable in cash or common shares. If a director elects to defer part of his or her retainer or fees in shares, then the number of shares credited to the director’s account is equal to the portion of the retainer or fee elected to be received in shares, divided by the fair market value of the shares on the first day of the period to which the retainer or fee relates. The portion of a fee that is deferred will be credited following each plan year to the respective director’s account as of the date it would have otherwise been paid. Nonemployee directors may elect to receive deferred shares in lieu of their annual equity award with the same three-year vesting requirements, if applicable. Amounts held in deferred cash accounts earn interest at the end of each quarter based on the Moody’s Corporate Average Bond Yield, or such other rate as may be fixed by the plan administrator. Deferred share accounts earn dividend equivalents at the end of each quarter based on any cash dividends we pay during the quarter, which dividend equivalents are credited to the accounts in the form of additional deferred shares. The amounts in the director’s deferral accounts, whether cash or shares, together with any deferred dividends, will be paid to the director in the form elected after such director’s death, disability, termination of service or change in control of Cliffs.

Cliffs has a trust agreement with KeyBank National Association relating to the Directors’ Plan in order to fund and pay our deferred compensation obligations under the Directors' Plan.

Director Compensation for 2013

The following table, supported by the accompanying footnotes and the narrative above, sets forth for fiscal year 2013 all compensation earned by the individuals who served as our nonemployee directors at any time during 2013.

|

| | | | | | | | | | | | | |

Name | Fees Earned or Paid in Cash ($) (1) |

| Stock Awards ($) (2) |

| | Change in Pension Value and Non-Qualified Deferred Compensation Earnings ($) |

| | All Other Compensation ($) (3) |

| | Total ($) |

|

S. M. Cunningham | 79,000 |

| 85,000 |

| | — |

| | 9,062 |

| | 173,062 |

|

B. J. Eldridge | 91,750 |

| 85,000 |

| | — |

| | 9,062 |

| | 185,812 |

|

M. E. Gaumond | 45,815 |

| 70,562 |

| | — |

| | 1,326 |

| | 117,703 |

|

A. R. Gluski | 78,500 |

| 85,000 |

| | — |

| | 4,491 |

| | 167,991 |

|

S. M. Green | 85,000 |

| 85,000 |

| | — |

| | 9,062 |

| | 179,062 |

|

J. K. Henry | 103,000 |

| 85,000 |

| | — |

| | 9,984 |

| | 197,984 |

|

S. M. Johnson | 23,500 |

| 50,767 |

| | — |

| | 366 |

| | 74,633 |

|

J. F. Kirsch | 333,750 |

| 835,000 |

| (4) | — |

| | 24,850 |

| (5) | 1,172,189 |

|

F. R. McAllister (6) | 70,500 |

| 85,000 |

| | 81 |

| (7) | 7,483 |

| | 163,064 |

|

R. K. Riederer | 91,000 |

| 85,000 |

| | — |

| | — |

| | 176,000 |

|

R. A. Ross (8) | 33,000 |

| — |

| | — |

| | 428 |

| | 33,428 |

|

T. W. Sullivan | 82,950 |

| 111,548 |

| | — |

| | 2,234 |

| | 196,732 |

|

| |

(1) | The amounts listed in this column reflect the aggregate cash dollar value of all earnings in 2013 for annual retainer fees, chairman retainers and meeting fees, whether received in required retainer shares, voluntary shares, cash or a combination thereof. Unless otherwise noted below, the amounts indicated were elected to be paid in cash during 2013. |

Mr. Eldridge and Ms. Cunningham met the Director Share Ownership Guidelines and elected to continue to receive $24,000 each in common shares. Messrs. Kirsch and Riederer met the Director Share Ownership Guidelines and elected to defer $24,000 in common shares pursuant to the Directors’ Plan.

| |

(2) | The amounts reported in this column reflect the aggregate grant date fair value computed in accordance with Financial Accounting Standards Board (or FASB) Accounting Standards Codification (or ASC) Topic 718 for the nonemployee directors’ annual equity awards of either restricted shares or unrestricted shares granted during 2013, which awards are further described above, and whether or not deferred by the director. The grant date fair value of the nonemployee directors’ annual equity award on May 7, 2013 was $21.33 per share ($85,000). Among the nonemployee directors, Mr. McAllister (who was 69 years of age or older on the annual meeting date in May 2013) received 3,985 unrestricted common shares as his annual equity award for 2013 under the Directors’ Plan. Mr. Riederer, who also was 69 years of age or older on the annual meeting date in May 2013, elected to defer his unrestricted shares under the Directors' Plan. Mr. Kirsch elected to defer his 3,985 restricted shares under the Directors’ Plan. Messrs. Kirsch, McAllister and Riederer have elected to defer their dividends on certain of their annual equity awards into additional common shares subject to the same risk of forfeiture as their original grants pursuant to the Directors’ Plan. As of December 31, 2013, the aggregate number of restricted shares subject to forfeiture held by each nonemployee director was as follows: Ms. Cunningham—6,408; Mr. Eldridge—6,408; Mr. Gaumond—4,421; Dr. Gluski—6,698; Ms. Green—6,408; Ms. Henry—6,408; Mr. Johnson—2,440; Mr. Kirsch—0; Mr. Riederer—0; Mr. Sullivan—4,720. As of December 31, 2013, the aggregate number of unvested deferred shares, including dividend reinvestments, allocated to the deferred share accounts of Messrs. Kirsch and Riederer under the Directors’ Plan were 2,953 and 20,635, respectively. |

| |

(3) | These amounts reflect dividends earned in 2013 on restricted share awards. |

| |

(4) | In addition to his annual equity grant in May 2013 of $85,000, Mr. Kirsch received a grant of 45,760 phantom stock units valued at approximately $750,000 when he became Chairman of the Board in July 2013. The grant date fair value of the phantom stock units on July 9, 2013 was $16.39 per share. The phantom stock units vested on January 2, 2014 and were settled with a cash payment. |

| |

(5) | This amount includes approximately $21,400 of housing expenses that Cliffs agreed to pay in 2013 while Mr. Kirsch was non-executive Chairman. |

| |

(6) | Mr. McAllister served as a director until June 2013. |

| |

(7) | Mr. McAllister recognized above-market earnings in his deferred cash account of $81. |

| |

(8) | Mr. Ross served as a director until April 2013. |

COMPENSATION DISCUSSION AND ANALYSIS

In this section, we discuss in detail our executive compensation program for 2013 for our named executive officers (or NEOs) consisting of our principal executive officers, our chief financial officer (or CFO), the next three highest paid executive officers employed as of December 31, 2013, and one former executive who served during 2013 and whose compensation would have qualified her as being among the next three highest paid executive officers:

| |

• | Gary B. Halverson, President & Chief Executive Officer. Mr. Halverson was elected President & Chief Operating Officer (or COO) and principal executive officer effective November 18, 2013. He was elected as our Chief Executive Officer (or CEO) effective February 13, 2014. |

| |

• | Terrance M. Paradie, Executive Vice President & CFO. |

| |

• | P. Kelly Tompkins, Executive Vice President, External Affairs & President, Global Commercial. Mr. Tompkins served as interim principal executive officer from October 21, 2013 until November 18, 2013. |

| |

• | Donald J. Gallagher, former Executive Vice President & President, Global Commercial, through December 31, 2013, at which time he retired from Cliffs. |

| |

• | Colin Williams, Senior Vice President, Asia Pacific Iron Ore. Mr. Williams' employment with Cliffs is expected to terminate on July 1, 2014. |

| |

• | William Hart, former Senior Vice President & Chief Strategy and Marketing Officer. Mr. Hart's employment with Cliffs terminated on March 25, 2014. |

| |

• | Joseph A. Carrabba, former Chairman, President & CEO. Mr. Carrabba served as principal executive officer until October 21, 2013. |

| |

• | Laurie Brlas, former Executive Vice President & President, Global Operations. Ms. Brlas retired during 2013. |

2013 Leadership Transitions

We experienced several executive officer transitions during 2013.

| |

• | Effective July 9, 2013, Mr. Carrabba stepped down as Chairman of the Board but remained our President & CEO until he retired effective November 15, 2013. He was our principal executive officer until October 21, 2013. |

| |

• | Ms. Brlas retired from her position as Executive Vice President & President, Global Operations effective July 31, 2013. |

| |

• | During the transition period from October 21 until November 17, 2013, Mr. Tompkins served as the principal executive officer of Cliffs. |

| |

• | On November 18, 2013, Mr. Halverson commenced serving as our President & COO and in a principal executive officer capacity. When he was hired, the Board's intent was for him to transition into the CEO role, and Mr. Halverson was elected as Cliffs' CEO on February 13, 2014. |

| |

• | Mr. Gallagher, our former Executive Vice President & President, Global Commercial, retired from Cliffs after nearly 33 years of service on December 31, 2013. |

As a result of these transitions, our Compensation Discussion and Analysis, or CD&A, and the related compensation tables and narratives cover eight NEOs for 2013 and analyze a variety of compensation decisions and actions, some of which were made specifically with regard to these transition events. Not all of the NEOs participated in or received all of the compensation elements described in this CD&A. For example, Mr. Halverson did not participate in some of the programs, such as the annual grant of performance shares and restricted share units, in which our other NEOs participated. When discussing each compensation element in this CD&A, we will explain the degree to which each NEO participated or was eligible for the program.

Mr. Halverson was offered the following compensation package for joining Cliffs in 2013: annual base salary of $950,000; annual incentive target of 120 percent of his base salary; and an annual long-term incentive target grant value of 375 percent of his base salary. This compensation package will be in effect for fiscal year 2014. In 2013, Mr. Halverson received a prorated salary and annual incentive opportunity. Additionally in 2013, Mr. Halverson received a sign-on award of $2.0 million, consisting of cash and equity, as an incentive to join Cliffs and as a partial replacement for forfeited compensation with Mr. Halverson's former employer. This compensation package was developed in consultation with our independent compensation consultant, Semler Brossy, in consideration of market best practices.

The following discussion focuses primarily on compensation actions taken and decisions made during our 2013 fiscal year, but also contains information regarding compensation actions taken and decisions made both before and after the fiscal year to the extent that such information enhances the understanding of our executive compensation program. It includes a description of the principles underlying our executive compensation policies and our most important executive compensation decisions for 2013, and provides analysis of these policies and decisions. The discussion gives context for and should be read together with the data presented in the compensation tables, the footnotes and the narratives to those tables and the related disclosures appearing elsewhere in this Form 10-K/A.

Say-On-Pay Implications

At our Annual Meeting of Shareholders in May 2013, only 66.3 percent of our voting shareholders voted in favor of our annual advisory vote on named executive officers' compensation, commonly referred to as “Say-on-Pay”. However, this was in sharp contrast to our May 2012 results, where our shareholders overwhelmingly approved our named executive compensation by voting 97.3 percent in favor. In response to the significantly lower year-over-year results, we identified that, along with others in 2013, two of our top shareholders voted against our Say-on-Pay proposal, which had a substantial impact on the decline in results. It should be noted that both of these top shareholders were also top shareholders in 2012, and both voted "for" our Say-on-Pay proposal in that year. Due to the fact we had not made substantial changes to our executive compensation program between 2012 and 2013, management and the Chairman of the Board of Directors engaged in direct face-to-face dialogue with these two shareholders. A key takeaway from the dialogue was that Cliffs' poor share price performance was a significant contributing factor to the shareholders' decisions to reverse their Say-on-Pay support in 2013.

Additionally, as part of a broader shareholder outreach program during early 2014, we reached out to our top 25 shareholders, which collectively held 59 percent of our shares outstanding at December 31, 2013. The purpose of this outreach was to gain insight into and perspective on our executive compensation programs and policies as disclosed

in our proxy statement for our 2013 Annual Meeting. Ultimately, in January 2014, we conducted telephone discussions with the holders of approximately 15 percent of our shares outstanding. During these interactions, we also highlighted some of the year-over-year changes in our corporate governance and executive compensation practices. Additionally, we addressed Cliffs' 2013 share price performance and discussed the recent changes with our Board of Directors and executive management. The feedback from these meetings was shared with and considered by management and the Compensation Committee when the executive pay programs were reviewed for 2014.

Although the low Say-on-Pay vote result in 2013 was due mainly to our poor share price performance, in September 2013, the Compensation Committee implemented the following corporate governance enhancements to the executive compensation program because of its ongoing efforts to ensure a strong alignment between executive compensation and company performance:

| |

• | The vesting of all future equity grants beginning in late 2013 are subject to "double-trigger" change in control equity acceleration, rather than "single-trigger" acceleration (in other words, double-trigger provides that, generally, equity is accelerated only following a qualifying termination of employment associated with a change in control or a failure to assume, continue or replace the awards in connection with the change in control). |

We increased the required share ownership multiple of base salary from 4.5x to 6x for the CEO and the COO under our Share Ownership Guidelines. We also increased the required share ownership multiple of base salary from 2.5x to 3x for senior and executive vice presidents under these same guidelines.

Executive Compensation Philosophy and Core Principles

The Compensation Committee has designed our compensation structure to help attract, motivate, reward and retain high-performing executives. The goal is to align pay with Cliffs’ performance in the short term through variable cash compensation based on measures of financial performance and operational and strategic excellence, and over the long term through stock-based incentives. Our compensation philosophy is to place a significant portion of compensation at risk based on our performance, and increase this portion of compensation that is at risk as the responsibility level of the individual increases, consistent with market practices. We also seek to balance this performance focus with sufficient retention incentives, including a competitive fixed salary and the use of time-based restricted share units in our long-term incentive program.

Our guiding compensation principles for 2013 were as follows:

| |

• | Align incentive pay, both short and long term, with results delivered to shareholders. |

| |

• | Design a simple and transparent incentive plan that focuses on absolute performance objectives tied to our business plan (including profitability-related and cost control objectives), relative performance objectives tied to market conditions (including relative total shareholder return, measured by share price appreciation plus dividends, if any), and performance against other key objectives tied to our business strategy (including safety, protection of our core assets and selling, general and administrative cost control). |

| |

• | Provide competitive fixed compensation elements over the short term (base salary) and long term (equity and retirement benefits) to encourage long-term retention of our executives. |

| |

• | Structure programs to align with corporate governance best practices (for example, elimination of gross-ups related to change in control payments, conversion to double-trigger change in control equity vesting for future equity awards, use of Share Ownership Guidelines and adoption of a clawback policy related to incentive compensation for our executive officers). |

In general, 2013 pay opportunities for existing officers were intended to deliver target total pay opportunity between the median and 75th percentile of the market in which we compete for talent in order to enable us to attract and retain the caliber of executive talent needed to meet our business and strategic objectives.

Oversight of Executive Compensation

The Compensation Committee administers our executive compensation program, including compensation for our NEOs. The specific responsibilities of the Compensation Committee related to executive compensation include:

| |

• | Overseeing development and implementation of our compensation policies and programs for officers, including benefit, retirement and severance plans; |

| |

• | Reviewing and approving elected officer compensation, including setting goals, evaluating performance and determining results with the independent members of the Board; |

| |

• | Determining the compensation of our CEO (or other principal executive officer) and recommending the independent members of the Board ratify the compensation of our CEO (or other principal executive officer); |

| |

• | Participating in succession planning for our CEO and other officers; |

| |

• | Overseeing our equity-based employee incentive compensation plans, including actual plan design related to operating and strategic performance objectives, and approving grants; |

| |

• | Overseeing regulatory compliance with respect to certain other compensation matters; |

| |

• | Reviewing and approving any proposed severance agreements, retention plans or other agreements; and |

| |

• | Retaining and managing its relationship with any external compensation consultant. |

When making individual compensation decisions for executives, the Compensation Committee takes a number of factors into account, including market pay practices, the individual’s performance, tenure and experience, overall Cliffs' performance, any retention considerations, the individual’s historical compensation and internal fairness considerations. These factors are considered by the Compensation Committee in a subjective manner without any specific formula or weighting.

Decisions and approvals relating to the CEO’s pay are made by the Compensation Committee in executive session, without management present, and are subject to ratification by the independent members of the Board. In assessing the CEO’s pay, the Compensation Committee considers our performance, the CEO’s contribution to that performance and other factors as described above in the same manner as for any other executive. The Compensation Committee approves the CEO’s salary, annual incentive payout (consistent with the terms of the plan as described below) and long-term incentive grants each year subject to ratification by the independent directors. A similar process was used when making pay decisions for Mr. Halverson in 2013.

The Compensation Committee retains an independent executive compensation consultant who is engaged by and reports directly to the Compensation Committee. The compensation consultant attends portions of or all of the Compensation Committee meetings at the request of the Compensation Committee, frequently meets separately with the Compensation Committee with no members of management present and periodically works separately with the Compensation Committee Chairman between meetings.

For 2013, the Compensation Committee retained Semler Brossy as its compensation consultant. Semler Brossy was retained directly by the Compensation Committee and has helped the Compensation Committee develop an appropriate agenda for performing its duties. In this regard, Semler Brossy advised and assisted the Compensation Committee in:

| |

• | Designing executive compensation programs that align with our business and strategic objectives and shareholder interests; |

| |

• | Identifying mining industry and general industry peers and identifying compensation surveys for the Compensation Committee to use to initially assess the appropriateness and competitiveness of our executive compensation programs; |

| |

• | Identifying appropriate pay positioning strategies and pay levels in our executive compensation programs; |

| |

• | Reviewing external trends and best practices in executive compensation; |

| |

• | Identifying emerging good governance practices for the Compensation Committee’s consideration; and |

| |

• | Providing recommendations and guidance on pay packages for new executive officers as part of our leadership transition during 2013. |

Additional services requested of Semler Brossy in 2013 included a review of the directors’ compensation practices at the request of the Governance and Nominating Committee. The additional services provided did not exceed a cost of $120,000. Semler Brossy performs no other services for Cliffs or our management except as requested by the Compensation Committee, the Governance and Nominating Committee or the Audit Committee. The independence

of Semler Brossy has been assessed by the Compensation Committee, as required under NYSE listing rules. The Compensation Committee also has considered and assessed all relevant factors, including but not limited to those set forth in Rule 10C-1(b)(4)(i)-(vi) under the Exchange Act, that could rise to a potential conflict of interest with respect to Semler Brossy. Based on this review, we are not aware of any conflict of interest that has been raised by the work performed by Semler Brossy.

Market for Talent

The Compensation Committee conducts an annual review of market pay practices for executive officers with the assistance of its outside compensation adviser. Semler Brossy conducted a review of market pay practices in late 2012 for 2013 executive compensation decisions. This review was based on several published compensation surveys, including Hewitt Associates’ and Towers Watson’s executive compensation general industry surveys, as well as a detailed proxy analysis of executive compensation among our compensation peer group.

The compensation peer group was last evaluated in September 2012 and, at Semler Brossy’s recommendation, the Compensation Committee approved the addition of Walter Energy, Inc. to the 2013 compensation peer group. The resulting compensation peer group used for the 2013 analysis included the following 20 companies:

|

| |

Agrium Inc. | FMC Corporation |

Airgas, Inc. | Goldcorp Inc. |

Air Products and Chemicals, Inc. | Kinross Gold Corporation |

Allegheny Technologies Incorporated | Mosaic Company (The) |

Alpha Natural Resources, Inc. | Newmont Mining Corporation |

Arch Coal, Inc. | Peabody Energy Corporation |

Celanese Corporation | Praxair, Inc. |

CF Industries Holdings, Inc. | Teck Resources Limited |

CONSOL Energy Inc. | Vulcan Materials Company |

Eastman Chemical Company | Walter Energy, Inc. |

At the time of the September 2012 assessment, the peer group had median revenue and market capitalization of:

|

| | | | |

| Revenue –

Trailing 4-Quarter Average

($ millions) | Revenue –

3-Year FYE Average ($ millions) | Market Value – 90-day Average

($ millions) | Market Value –

3-Year FYE Average ($ millions) |

Peer Group Median | 6,557 | 4,869 | 7,106 | 8,650 |

Cliffs | 6,696 | 4,612 | 7,229 | 8,486 |

Source: S&P Research Insight | | | |

Pay Mix

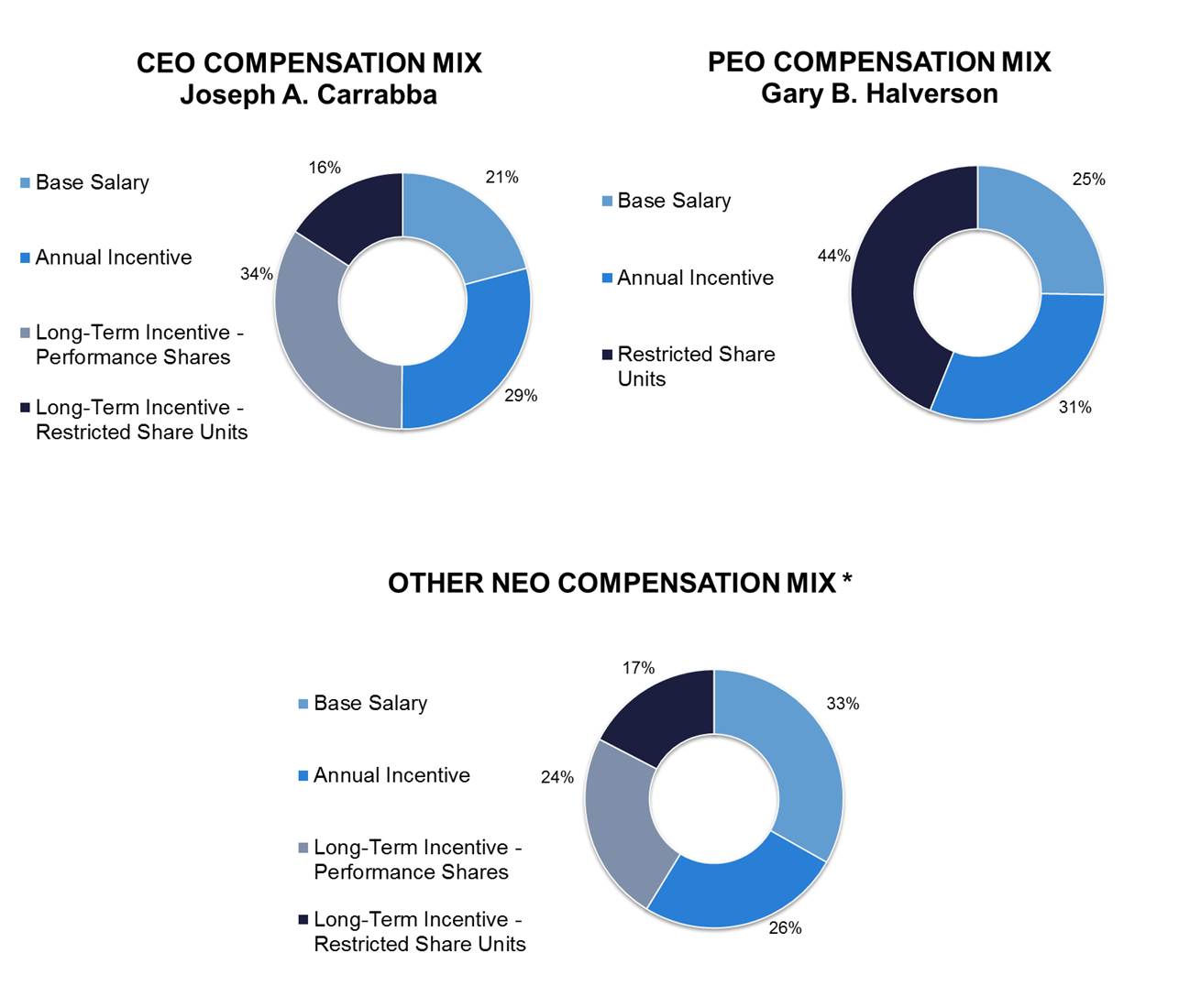

Because our executive officers are in a position to directly influence our overall performance, a significant portion of their compensation is variable and aligned to our short- and long-term goals and shareholder interests. The variable pay components include the annual incentive (cash-based) and long-term incentive (equity-based) awards. Approximately 79 percent and 75 percent of Mr. Carrabba's and Mr. Halverson's total target compensation, respectively, and approximately 67 percent of the other NEOs’ total target compensation is variable for 2013 as illustrated by the charts below. Additionally, half of our CEO’s pay and more than one-third of the other NEOs' pay is delivered in the form of long-term compensation. The levels of performance-based variable pay are consistent with each executive’s level of responsibility and impact and are consistent with market practices for fixed versus variable pay.

|

| | | | | | | | | |

| 2013 Target Pay Mix* | |

Base Salary |

| Annual Incentive |

| Performance Shares |

| Restricted Share Units |

| |

Halverson | 25 | % | 31 | % | — |

| 44 | % | (1) |

Paradie | 36 | % | 29 | % | 24 | % | 11 | % | |

Tompkins | 25 | % | 20 | % | 17 | % | 38 | % | (2) |

Gallagher | 33 | % | 26 | % | 28 | % | 13 | % | |

Williams | 38 | % | 27 | % | 24 | % | 11 | % | |

Hart | 43 | % | 31 | % | 18 | % | 8 | % | |

Carrabba | 21 | % | 29 | % | 34 | % | 16 | % | |

Brlas | 33 | % | 26 | % | 28 | % | 13 | % | |

* Figures have been rounded and exclude any sign-on cash award, severance, retirement or superannuation payments made in 2013.

(1) Includes a new hire grant of restricted share units on November 18, 2013.

(2) Includes a retention grant of restricted share units on November 11, 2013. | |

* Mr. Tompkins' compensation is included in the Other NEO Compensation Mix

Principal Elements of our 2013 Compensation

During 2013, our executive compensation and benefits primarily consisted of the components listed in the following table, which provides a brief description of the principal elements of compensation, how performance factors into each type of compensation and the objectives served by each element. These elements are discussed in more

detail in the sections that follow.

Fiscal Year 2013 Principal Compensation Elements

|

| | | |

Element | Description | Performance Conditions | Primary Objectives |

Base Salary | Fixed cash payment | Based on level of responsibility, experience and individual performance | Attraction and retention |

EMPI Plan | Short-term incentive (annual cash payment) | Based on EBITDA, volume, cost control initiatives and strategic performance objectives | Motivate the achievement of short-term strategic and financial objectives |

Performance Shares | Long-term incentive (equity-based payment) | Based on TSR relative to a peer group | Attraction, retention and promotion of long-term strategic and financial objectives and long-term share performance |

Restricted Share Units | Long-term retention (equity-based payment) | Value related to share performance | Attraction, retention and promotion of long-term share performance |

Retirement and Welfare Benefits | Health and welfare benefits, deferred compensation, 401(k) company contributions, superannuation, defined benefit pension participation and supplemental executive retirement plans | — | Attraction and long-term retention |

Executive Perquisites | Financial services and company-paid parking | — | Avoid distraction from Cliffs’ duties |

Analysis of 2013 Compensation Decisions

Base Salary